China's real estate market has long been a symbol of economic growth and prosperity. Over the past few decades, China's rapid economic development has fuelled a massive real estate boom, leading to soaring property prices and a construction frenzy. However, recent events have cast a dark shadow over the industry and concerns over a potential bubble have been mounting as housing affordability rapidly deteriorates, speculative investment rises, and developers accumulate unaffordable levels of debt.

In 2021, Evergrande—one of China’s largest real estate developers, overseeing projects in 200 cities—stumbled into a debt crisis. With a staggering debt load exceeding $300 billion1 and a liquidity crunch, Evergrande struggled to meet its debt obligations. Offshore bond payments of $83.5 million and three additional payments totalling $148 million faltered within just three weeks1, leaving domestic and international investors anxious. Fitch, a financial risk ratings agency, eventually declared Evergrande in default.

Evergrande’s aggressive expansion strategies and absurdly high leverage had pushed it into a corner, exposing the fragility of a sector that was once the poster child of China’s economic boom. The Evergrande crisis served as a wake-up call, forcing the Chinese government to take swift action to prevent a systemic collapse. China’s interventions included urging local governments to ensure stability, encouraging debt restructuring and tighter regulation for property developers. Whilst these measures provided temporary relief, they underscored the urgent need for a more sustainable approach to the real estate sector.

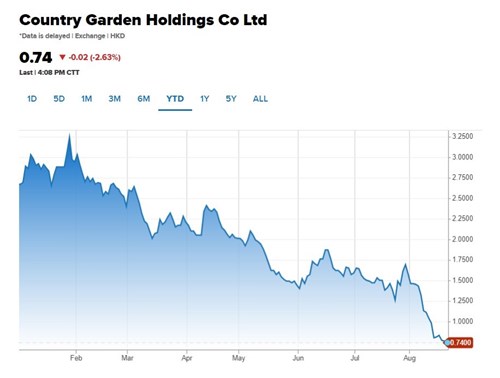

Fast forward two years and as the echoes of the Evergrande debacle continue to resonate, another real estate giant, Country Garden Holdings (one of the largest Chinese developers by revenue and named in Forbes’ list of the top 500 companies in the world), said it had missed an August 7th deadline for making a $22.5 million repayment on two US dollar-denominated bonds2. Moreover, days later, the company announced a net loss of up to 55 billion yuan ($7.6 billion) for the first half of the year, compared with a net profit last year of 1.91 billion yuan ($265 million)3. The company said trading on 11 of its onshore bonds would be suspended, starting Monday. The company is now grappling with similar challenges that once plagued Evergrande. Rapid expansion (fuelled by aggressive leverage) has left investors concerned about the stability of the company’s financial position – a situation akin to "Evergrande 2.0".

Source: CNBC

Country Garden Holding’s situation serves as a stark reminder that the issues that led to the Evergrande crisis are not isolated incidents, but rather symptoms of deeper structural problems within China’s real estate sector. There is always the worry that the problems faced by Evergrande and Country Garden Holdings are not confined to the walls of their businesses. The current situation at Country Garden highlights that the problems of China’s property developers are only getting more severe. After a small reprise in early 2023, developer financing flows have turned downwards. The review of financial reports of those listed developers doesn’t paint a good picture with many of their cash and liquidity positions deteriorating and rising losses putting many at risk of insolvency. Nearly half of all listed private developers reported earnings before interest, taxes, depreciation, and amortisation of less than their interest payments in 2022, a standard indicator of liquidity risk.

The potential impact on the global economy explains why policymakers are taking more steps (extending help to developers with debt maturing before the end of 2024 – an extension to the previous May 2023 maturity deadline) to support developers and stabilise housing sales.

Promisingly, recent hints from policymakers suggest they are poised to further try and stimulate property sales. Following a recent political meeting, the housing ministry called for reductions in down payment ratios and lower mortgage rates for first-time buyers, alongside tax cuts for those upgrading their primary residences. While major cities may experience sentiment shifts from such relaxations, no specific measures have been announced by local officials in this regard.

The absence of specific measures raises uncertainties about potential support for the property market. Without intervention, property sales figures are likely to keep declining, and concerns of contagion could materialise.

While we are structurally cautious about direct investment in China, importantly for you, our clients, we have no company specific exposure to Country Garden Holdings across any of our strategies and we continue to keep abreast of the challenges facing the Chinese Real Estate sector to ensure minimal/no exposure in all portfolios.

We wish you a good week. Please note that, due to the summer bank holiday, the next update will be on Tuesday 29th August.

Sources: