Investment diversification is used here to describe the manner in which we invest in different asset classes to make up an investment portfolio, although the phrase may also be used to describe the manner in which we spread our risk within each asset class.

- Property: our house, but also buy-to-let residential and commercial buildings;

- Bonds: debt instruments that, say, governments or companies issue to borrow our money and promise to pay it back later, usually at a specified date and with a periodic coupon* paid on the nominal amount we own;

- Equity: shares in a company that entitle holders to vote at meetings and to dividends*, if paid;

- Gold: shiny bars and coins;

- Cash: cash at our retail bank where we have a credit balance (that is to say that we are creditors of the bank and they owe us the money);

We can invest directly in any of those or through a fund* that has the required exposure.

Starting at the end

Investment is based on risk and reward, with our understanding that the more we take of the former, the more that we will, ultimately, expect to receive of the latter* … and this is generally and fundamentally the case because of what I like to call, “The Grim Reaper’s Batting Order”; a hierarchy that determines which group of creditors* is paid first during an insolvent liquidation of a company.

Those owed money in this scenario are ranked as follows, and each class of creditor must be paid in full before any remaining company funds are allocated to the next:

- Secured creditors with a fixed charge;

- Preferential creditors;

- Secured creditors with a floating charge;

- Unsecured creditors; and

- Shareholders.

So back to the plot

Diversification of investment in bonds and equity therefore allows us to occupy more than one position on the list. Diversification into more than one company, sector or region* allows us to occupy more positions on more lists and that sounds sensible, right?

Concluding, and quickly

Of course, if we knew into which basket to put all our eggs, we would do it tomorrow. We don’t and therefore should continue to employ asset allocation which suits our personal circumstances (age, stage, wage and objectives).

Under what is known as modern portfolio theory, we can reduce the overall risk of our portfolio, and actually increase our overall returns, by investing in asset combinations that are not correlated: that is to say that they don't tend to move in the same way at the same time. And let’s regard 2020, by most metrics, as an extraordinary time.

Investment in property, aside from our home, is normally made with a view that prices will rise and that tenants, if applicable, will pay their rents. This view may have changed, in the short-term, at least, depending on where the property is and who those tenants are.

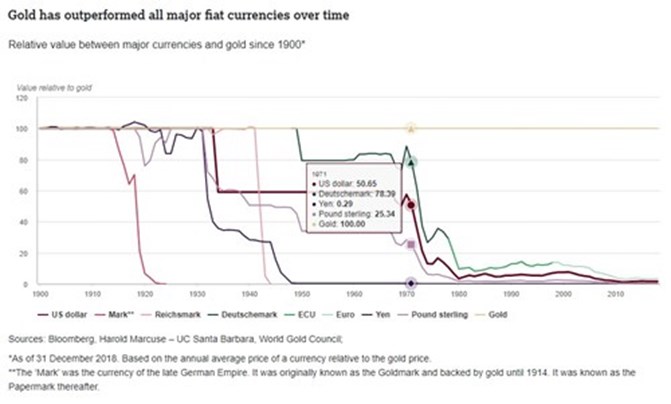

Gold can provide us with one of the few ‘counterparty-free’ assets. Investment rationale has always been the same: that the yellow metal tends to perform well in times of geopolitical unrest, during economic slowdown and when global interest rates and bond yields low or negative and when supply is disrupted. Central Banks, one of the major ‘players’ in the gold market, have been net buyers of gold since 2008, with their greatest investment since 1971 (when the gold standard was effectively abandoned) made in 2018 and 2019 **

Cash is subject to the risk of the bank and its solvency, and will only thrive in periods of deflation (when prices of goods in the future actually become cheaper). More interesting will be how fiat* currencies react to the unprecedented levels of ‘printing’ that have been employed and further promised by governments willing to do “whatever it takes” to end the current potential economic crisis.

Having mentioned 1971 above, it might be worth our noting the below:

So now you know why most commentators, including this one, usually end their notes with “as usual, we would recommend you to stay invested in a diversified portfolio, kindly note that the value of investments and the income derived from them may go down as well as up and you may not receive back all the money which you invested. Any information relating to past performance of an investment service is not a guide to future performance.”

All that said, it might be the right time, now, for us to (re)consider that we are still comfortable with all of our holdings. Trusted professionals will tell us, and it’s a phrase used by Ravenscroft and BullionRock many times, to know what we own and why we own it.

* noting, without exaggeration, that each time an asterisk has been used in this piece, a further 400 words on that specific point could easily be written

** from The World Gold Council “Central bank net purchases in 2019 were remarkable. The annual total of 650.3t is the second highest level of annual purchases for 50 years, highlighting the importance central banks place on having an allocation to gold in their reserve portfolio. The highest level was recorded in 2018 and buying in 2019 was not widely expected to repeat these levels for a second consecutive year” https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2019/central-banks-and-other-institutions